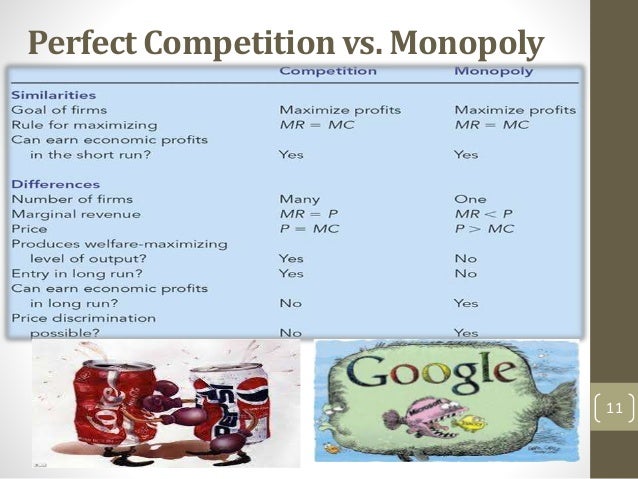

In a purely competitive market, each firm's production is such a small proportion of industry output that a single firm has no influence on the market price. We can define four conditions that characterize a purely competitive market:

Firms in a purely competitive market sell a homogeneous product. That is, they sell identical or nearly identical product that are perfectly substitutable for one another. This means that advertising does not exist in a purely competing firms. Why would one firm want to advertise the advantages of its product if cannot be distinguished by consumers from the products produced by a large number of competing firms?

A large number of independent buyers and sellers exist in a purely competitive market. This assumption rules out the possibility of collusion among buyers and sellers to affect price and output in the industry. Moreover, the large number of buyers or seller will not affect the market price. Each buyer and seller is small relative to the totoal market for the commodity and experts no perceptible influence on the market.

Because buyers and sellers in perfectly competitive markets must accept the price the market determines, they are said to be price takers.

There are no barriers to entry or exit in a purely competitive market. Features of economic life such as control of an essential raw material by one or a few firms or government regultion of firms’ behaviour in the market do not exist under pure competition.

A perfectly competitive market also offers perfect information to buyers and sellers. Everybody in the market has equal, free access information about the location and price of a product. This assumption provides the basis for a single price to prevail in a perfectly competitive market. Buyers and sellers are constantly informed about the price difference and act in turn to drive industry price to a single value.

The opposite extrem to a purely competitive firm is a pure monopoly: a single seller in an industry. The pure monopoly, in fact is an industry. It alone can affect market price by changing the amount of output that it produces. Threfore, the pure monopoly is referred to as a price searcher. It must seek the price that maximize its profits. It is an industry composed of a single seller of a product with no close substitutes and with high barriers to entry.

Examples of pure monopoly in the sense of a single seller in an industry are rare. In 16th and to 18th century Europe, monarch granted monopoly rights to undertakings. These were pure monopolies because each was given the exclusive right to run an entire industry. For example, the king of England created only one English Eeast India Company, which was empowered with a monopoly over the trade with India. This monopoly power was manifested in the high prices the East India Company charged for the goods it brought back from India and sold in England.

Even in these historical cases of monopoly, the monopoly was usually granted to a group of merchants, who were, therefore, not technically a single seller, but rather a group of sellers acting as a single seller.

A second problem in applying the definition of monopoly concerns the criterion that there be no close substitutes. All products exhibit some degree of substitutability. The monopolist's isolation from competition from substitute products is threfore a matter of degree. Where there are close substitutes, the monopolist cannot substantially raise prices without losing sales. Where there are no close substitutes the monopolist has more power to raise prices.

A third consideration in defining monopolies is high barriers to new entry by potential competitor, the basis source of a pure monopoly. There are several types of barriers to new competition: legal barriers, economies of scale, and control of an essential resource.

Economic of scale-the property whereby long-run average cost falls as the quantity of output increases.

Diseconomies of scale-the property whereby long-run average cost rises asthe quantity of output increases.

Legal monopoly- (de jure monopoly)- based on laws explicitly preventing competition

- Government monopoly (state monopoly)

Efficiency monopoly- a single firm is satisfying all consumer demand

Natural monopoly –when economies of scale are so large that a single firm can supply the entire market without exhausting them

Coercive monopoly- arises as the result of any sort of activity that violates the principle of a free market

Monopoly (one single seller) – from the Greek monos (one) and polein ( to sell)

Monopolistic competition- near monopoly, de facto monopoly (dumping products below cost to harm competitors, creating trying arrangements berween their products, and other practics regulated under antitrust law)